Are you tired of feeling like accounting is a foreign language? Do words like receipt and payments account make your head spin? Don’t worry, you’re not alone. Accounting can be confusing, but there are some golden rules that can help simplify things. By understanding these basic principles, you’ll be well on your way to mastering the world of finance. So let’s dive into the three golden rules of accounting!

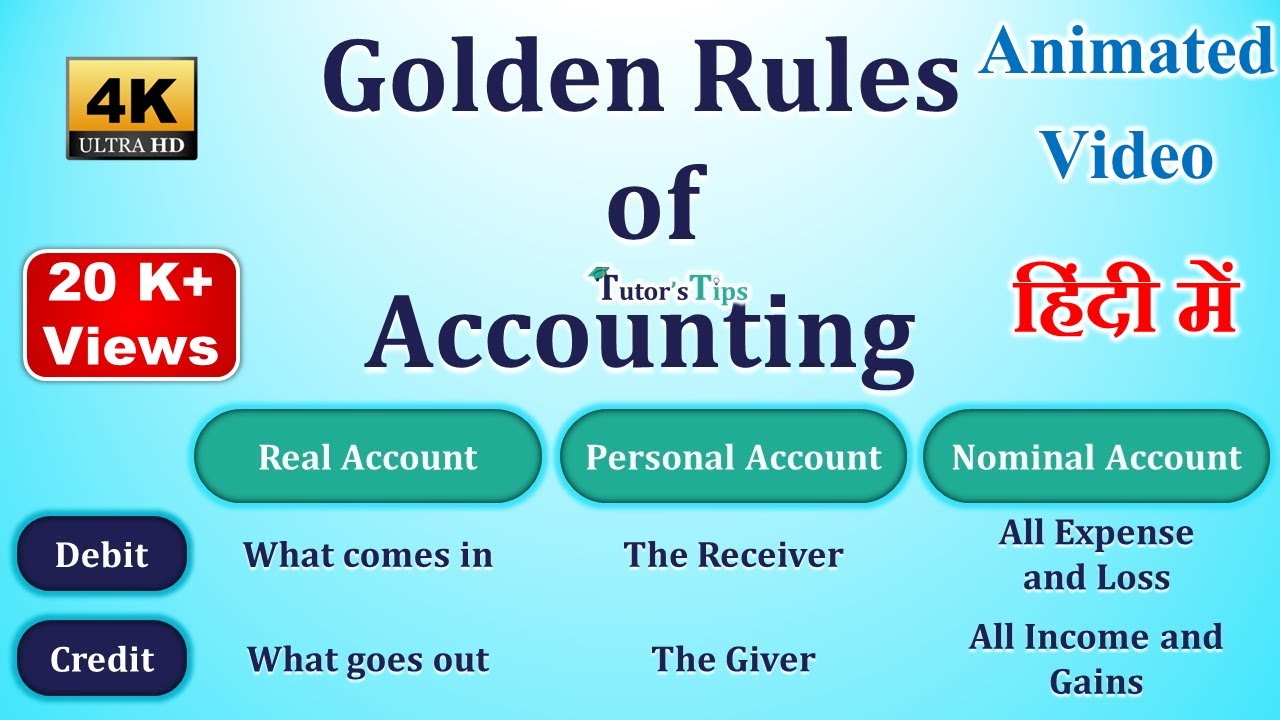

Debit the receiver and credit the giver

When it comes to accounting, the first golden rule is to “debit the receiver and credit the giver.” This simply means that when a transaction occurs, one account will be debited and another credited. But how do you know which account should be debited or credited?

Think of it this way: if money is being received, then debit the account that receives it. Conversely, if money is being given out or paid, then credit the account that gave it. For example, if a company sells merchandise and receives payment from a customer, they would debit their cash account (because they received money) and credit their sales revenue account (because they earned income).

But what about non-monetary transactions? The same principle applies. If goods are received instead of money, then debit the inventory or supplies account (the receiver), and credit accounts payable (the giver). By following this simple guideline, you can ensure accurate bookkeeping records for your business.

It’s important to note that while this rule may seem straightforward at first glance, there are exceptions based on specific transactions. Additionally ,this rule only applies in double-entry accounting systems – but more on that later!

Debit what comes in and credit what goes out

In the world of accounting, there are certain rules that every individual should know in order to record financial transactions accurately. One such rule is “debit what comes in and credit what goes out.” This principle is also known as the Real Account Rule.

To understand this concept better, let’s take an example. Suppose you receive cash from a customer who has purchased goods from your store. In this case, you would debit (record on the left side of the ledger) cash since it has come into your business and credit (record on the right side of the ledger) sales account because goods have gone out of your business.

Similarly, if you pay rent for office space or purchase inventory for sale, you would debit rent expense or inventory account respectively because they have gone out of your business and credit cash since it has come into your business.

This rule is essential when creating accurate financial statements such as balance sheets and income statements since incorrectly recorded transactions can lead to misinterpretation.

Understanding how to apply “debit what comes in and credit what goes out” is crucial when keeping track of financial records within a company.

Debit expenses and losses, credit income and gains

Accounting may seem daunting at first, but by following these three golden rules of bookkeeping, you can simplify the process and ensure accurate financial reporting. By remembering to debit the receiver and credit the giver, debit what comes in and credit what goes out, as well as debit expenses and losses while crediting income and gains – you’ll be on your way to mastering basic accounting principles.

Remember that the golden rules of accounting are essential for any business or organization aiming to succeed financially. Accurate record-keeping helps track profits, cash flow management, assist with decision-making processes and much more. It’s important not to overlook it! With a little practice in applying these fundamental guidelines of accounting every day can lead to becoming an expert soon enough!