Many people dream of retiring. Hopefully, they’re finding their career fulfilling, but that doesn’t mean they will want to stay in it forever. Most individuals would like to enjoy their Golden Years when they reach their life’s later stages.

If you have this mindset, you should know about the retirement bucket strategy. The name is a little whimsical, but this is a technique that many people use, and it can pay serious dividends. We’ll talk about it in detail right now.

What is the Retirement Bucket Strategy?

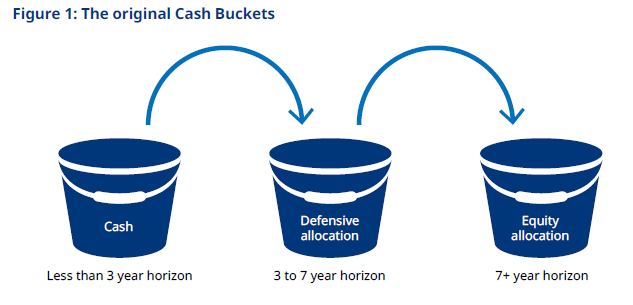

The retirement bucket strategy is a kind of investment approach. The idea is that you separate your income sources into three “buckets.” Those buckets are short-term, intermediate, and long-term financial goals.

Because this strategy involves saving, you’ll probably need to eliminate or reduce any outstanding debt you have before you attempt it. You can’t lock up much of your money and save it for retirement if you have pressing debts to deal with first. Consider using a snowball method calculator or a similar tool to reduce or eliminate debt before implementing the retirement bucket technique.

The Immediate Bucket

If this strategy interests you, the first thing you’ll want to do is set up the immediate bucket. This is where you will keep your cash or other liquid investments.

Short-duration T-bills would go in this bucket, as would high-yield savings accounts or US T-bills. What you want in this bucket is either money that you can readily access or short-term assets that you can convert to cash at a moment’s notice.

This bucket should have up to approximately two years of expenses in it. Some of this money might earn interest, but that’s not its primary goal; you want it more for any immediate expenses that come up.

The Intermediate Bucket

Next, you’ll set up the intermediate bucket. These funds should cover years 3-10 of your retirement. You want this money to grow so that it keeps pace with inflation. You won’t want to put any of it into high-risk assets, though.

This bucket might have CDs, REITs, utility stocks, income and growth funds, convertible bonds, or preferred stocks. If you speak to a financial professional, they can explain which of these options makes the most sense for you. Make sure to check the best stocks to buy today to find new investments.

The Long-Term Bucket

The long-term bucket should contain assets that historically grow your nest egg faster than the inflation growth rate. This is where you’ll have riskier assets. They should have growth potential over ten years or more.

Here you’ll have a diversified portfolio consisting mainly of stocks and related assets. The allocation might include large-cap and small-cap stocks, international and domestic investments and sustainable investments. If you need to, you can always liquidate some of these to refill the immediate and intermediate buckets if you have to drain them.

Many People Utilize This Strategy

Many financial consultants feel that this strategy works. It’s appealing because it has contingencies for the moment you retire, the next few years after that, and multiple decades into the future.

Remember, the short-term bucket is where you’ll have cash and short-term assets that you can quickly convert to cash if needed. The intermediate bucket is where preferred stocks, convertible bonds, CDs, and similar investments go that you’re hoping will keep pace with inflation.

The long-term bucket should contain riskier investments, like small and large-cap stocks. However, you’ll also want some diversification with this bucket, so you won’t take too much of a loss if one of the stocks tanks. Your long-term bucket is for investments with more than a decade of growth potential.

If this strategy intrigues you, you might reach out to a financial advisor to learn more. There are all kinds of retirement investment strategies, but most people consider this one measured and sensible.